Foreclosure Basics: Foreclosure is a legal process that allows a lender to take control of and sell your property if you fail to repay your loan. In California, there are two main types of foreclosure: non-judicial and judicial.

Types of Foreclosure:

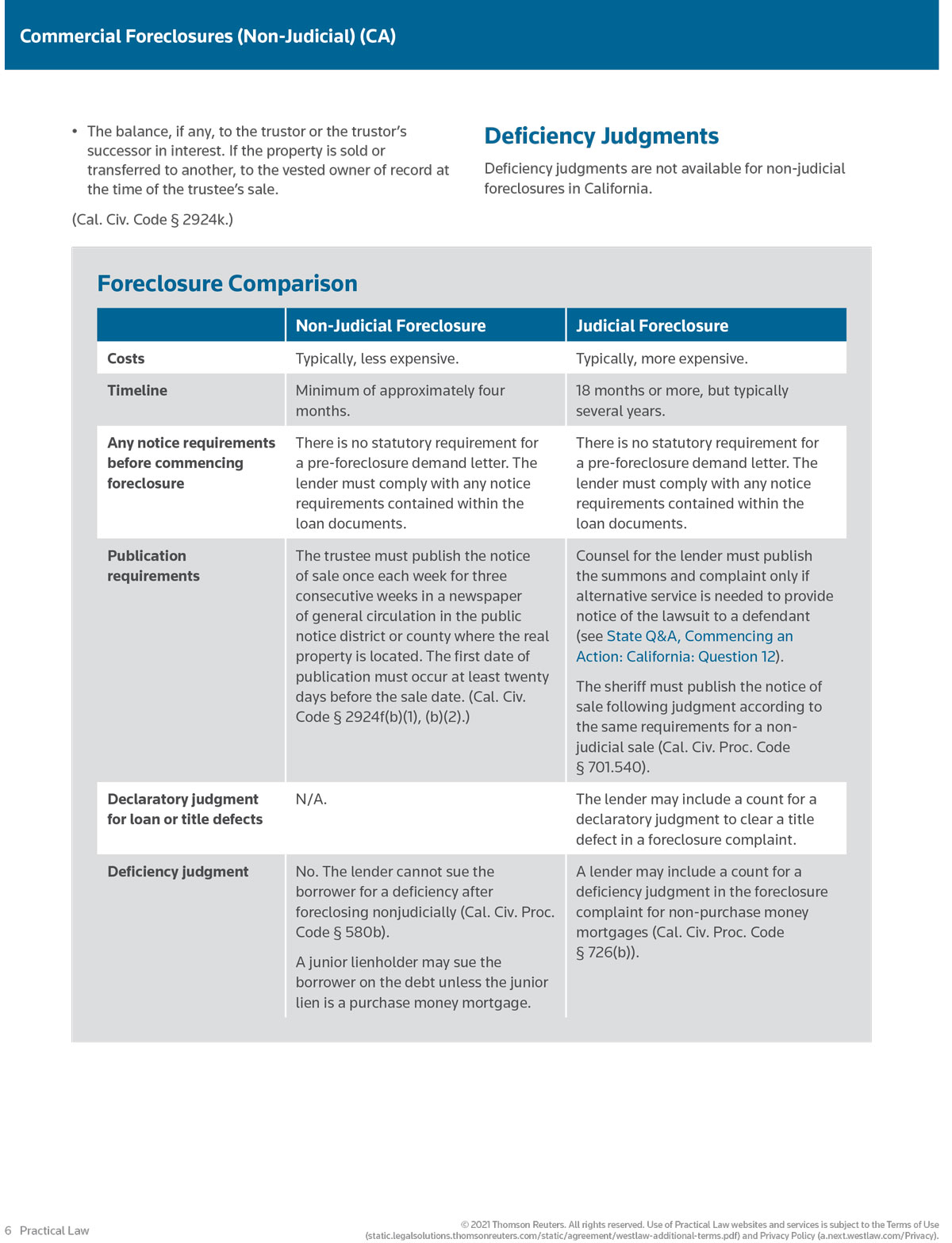

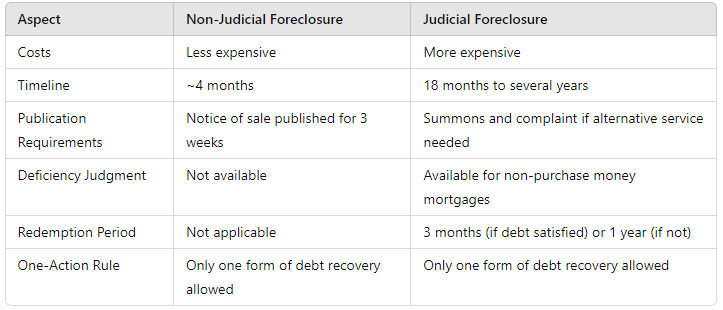

Non-Judicial Foreclosure:

Common Method: Most lenders in California use this method because it’s faster and less expensive.

How It Works: The process happens outside of court, typically through a public auction.

Legal Basis: Governed by the California Civil Code (§§ 2923.3 to 2944.10).

Judicial Foreclosure:

Less Common: Used less frequently because it involves going through the court system, which can be lengthy and costly.

How It Works: The lender files a lawsuit, and if successful, the court orders the sale of the property.

Legal Basis: Governed by the California Code of Civil Procedure (§§ 725a to 730.5).

Key Steps and Considerations for Non-Judicial Foreclosure:

Pre-Foreclosure:

Review Loan Documents: Ensure all terms and required notifications are understood.

Demand Letter: The lender usually sends a letter detailing the loan terms, the default, and what must be done to avoid foreclosure.

Title Search: The lender checks for other liens or claims on the property and ensures no bankruptcy filings halt the process.

During Foreclosure:

Substitution of Trustee: If the original trustee cannot conduct the sale, a new trustee is appointed.

Notice of Default: This is the formal start of the foreclosure process. The lender records and sends a notice to you and any other interested parties.

Notice of Sale: After 90 days, the sale date is set, and a notice is prepared and distributed, detailing the auction time and place.

Auction Sale:

Public Auction: The sale happens between 9:00 a.m. and 5:00 p.m., Monday through Friday.

Bidding: Potential buyers, including the lender, can bid. The highest bidder wins, provided they can immediately pay the full bid amount.

After the Sale:

Trustee’s Deed: The trustee issues a deed to the winning bidder within 18 days.

Taking Possession: The new owner can take possession immediately if the property is vacant or after an eviction process if it’s occupied.

Proceeds Distribution: Sale proceeds are distributed to cover the sale costs, repay the lender, and settle any junior liens. Remaining funds go to the borrower.

Your Rights as a Borrower:

Reinstatement: You can stop the foreclosure by paying the overdue amounts and associated costs up to five business days before the sale.

Redemption: Unlike judicial foreclosures, you don’t have the right to reclaim your property after a non-judicial foreclosure sale by paying off the debt.

Anti-Deficiency Rules: In non-judicial foreclosures, the lender cannot seek additional payment from you if the sale doesn’t cover the full loan amount.

Why This Matters: Understanding these procedures helps you know what to expect and explore possible options to avoid foreclosure. If you’re facing foreclosure, consulting with an experienced attorney can provide guidance tailored to your situation.

Feel free to ask any questions or discuss any concerns you might have. We’re here to help you navigate this challenging process.

We have 34 years of combined experience in real estate, real estate investment, and foreclosure law. We place an emphasis on quality work coupled with quality client retention.